A famous investing adage goes:

“Concentrated bets grow wealth. Diversification preserves wealth”

Going all-in on Bitcoin was the concentrated bet that changed my life. It turbo-charged my net worth from a quarter of a million to nearly five million. It was the best-performing asset of the past decade, and I still believe it has plenty of room to run. On a CAGR basis, I expect it to continue outpacing most other assets.

But the volatility and lack of yield make Bitcoin a tricky asset to hold through retirement. As I wrote in my article on dividends, the goal should always be total portfolio return. Dividends are basically savvy accounting. But psychologically, they feel like freedom. In practice, there’s real psychological comfort in living off cash flow rather than selling down principal.

Bitcoin can drop 70–80% in a year. If your retirement plan is selling BTC to fund monthly expenses, a crash means selling off much more coin at much lower prices. That is a recipe for anxiety.

The solution is compromise. My post-FIRE portfolio is designed to last decades, produce reliable yield, and still keep me aggressively exposed to growth.

Ground Rules

- All funds are in USD. This is the global reserve currency and keeping everything in USD simplifies things

- Any funds that yield a dividend are Irish domiciled. This reduces the US Withholding tax on dividends from 30% to 15% and applies it only to US domiciled equities.

- Portfolio numbers are modelled with a nominal five million dollar portfolio value.

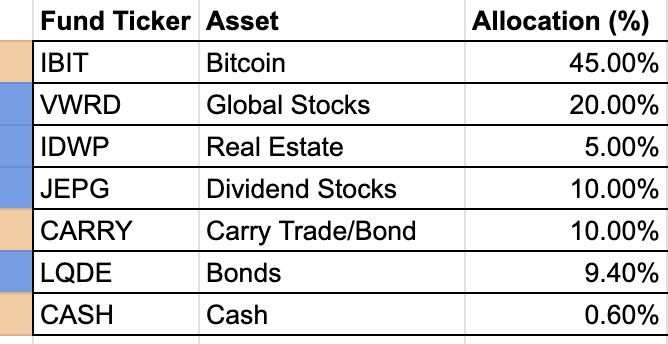

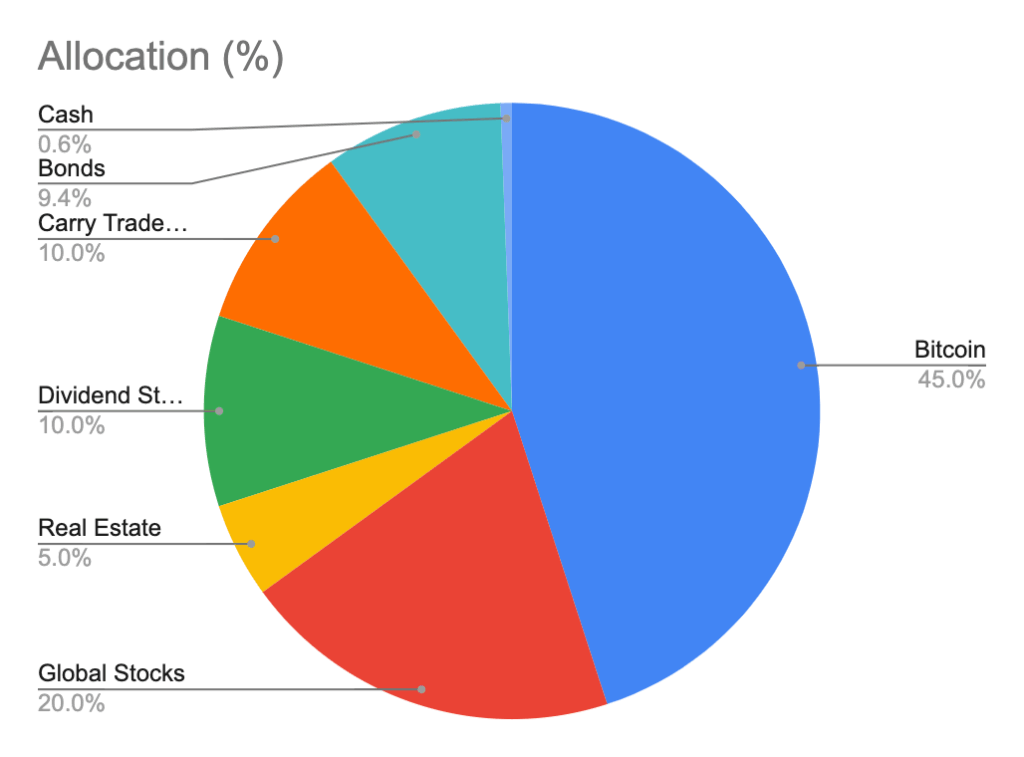

Bitcoin – 45%

First off, the largest single portion of the portfolio remains Bitcoin. Whilst this has been previously held personally in multi-signature cold storage, I do think that moving this over to simply holding the Blackrock $IBIT ETF is likely a good long term move. This bolsters my AUM at my brokerage, which both moves me up the VIP tier to reduce my cost of borrowing, and also increases the amount I can borrow via lombard loan against the portfolio. Bitcoin has no yield and is a pure growth play. It is uncorrelated to the other assets in the portfolio and retaining it at 45% of the overall mix should allow me to continue to capture massive upside from the asset class that has served me so well this far.

Global Equities – 20%

The next biggest chunk of the portfolio is Vanguard’s global equities ETF $VWRD. Almost the polar opposite to bitcoin (Vanguard still bans access to Bitcoin ETFs on their platform) this global equities ETF holds equity in some 3,500 of the worlds largest public companies. This is the boring index fund staple of most portfolios, and gives exposure just to the broad global stock markets. Typically it should grow around 7% per year and over the last 12 months it threw off around 1.5% in dividends.

Real Estate Investment Trust – 5%

Next up we have a 5% allocation to a global REIT (Real Estate Investment Trust), iShares $IWDP. This is another uncorrelated asset from both bitcoin and equities and yields around 4% per year in dividend cash flow. This fund owns millions of units of real estate across the world, from commercial (malls), to industrial (warehouses), to healthcare (hospitals), to residential (houses), and much more. The rent collected on these units is mandated in law to be passed on to the fund holders via quarterly dividend payments. This makes this slice of the portfolio an uncorrelated asset that also has a healthy cash flow.

High Yield Dividend Fund – 10%

Another 10% is allocated to a high dividend paying fund from JP Morgan, the $JEPG ETF. This is an actively managed fund that executes a covered call selling strategy on global equity markets and takes in large sums in premiums, giving up some of the growth upside in the stock market as the trade off. The previous 12 months have seen very anemic growth of just under 0.6%, but the fund throws off around 7-8% a year in free cash flowing dividends. This is large and provides several thousands of dollars of income replacement each month to fund cost of living. The nature of the fund and its covered call selling strategy also make it broadly uncorrelated with any of the other slices of the portfolio. Another win of an uncorrelated cash flow yielding slice of the portfolio.

Carry Trade – 10%

This section of the portfolio is actually neither a fund nor an asset, but instead a particular trade set up that acts as a high yielding bond of sorts. The key premise here is that you can exploit the difference between the spot price of an asset today and the long dated future price of the asset. This captures the gap between the two whilst keeping the overal trade fully hedged and directionally neutral. In simple terms, if we imagine the price of bitcoin is trading at $100k, and the futures contract for bitcoin a year from now is trading at $110k, the trade would be simply to buy 1 bitcoin and then short the $110k futures contract. Wait a year until the point of the futures expiry and you will be sitting on $110k in that trade, from $100k outlay, a return of 10%. The yield here varies depending on how exuberant the market is, but a yield of around 10% here is probably a good benchmark. This makes this slice of the portfolio entirely uncorrelated to anything, and heavily yielding cashflow.

Bonds – 9.4%

The final substantial chunk of the portfolio is filled with bonds. Bonds are boring as fuck. You essentially just lend money to companies and they pay you back with interest. The good thing about bonds is they are typically inversely correlated with equities. When stocks crash, bonds typically grow and money flees risky stocks into bonds. This helps smooth out volatility in the portfolio, and the ETF of choice for me is iShares $LQDE which yields just shy of 5% a year. Another non-correlated, cash yielding portion of the portfolio.

Cash – 0.6%

Finally, just straight cash. Roughly three months of day to day living expenses parked in cash, held on my coinbase account in stablecoins earning 12% interest. This creates a good buffer for daily spending and can be drawn down over the quarter as dividends and yield from investments builds over the quarter and then flow into the cash reserve topping it back up to three months of cash reserves at the start of each quarter. This gives fairly ample reserves to make large purchases if required and ringfences daily spending into an account separate from the rest of the portfolio, allowing that to continue to grow and yield income quarter after quarter.

To round out the portfolio I may look at adding gold, in some small allocation, or potentially a broader basket of commodities. One fund I like for this is iShares $ICOM, but as they are non yielding and the portfolio is quite well diversified, I think it’s good for now.

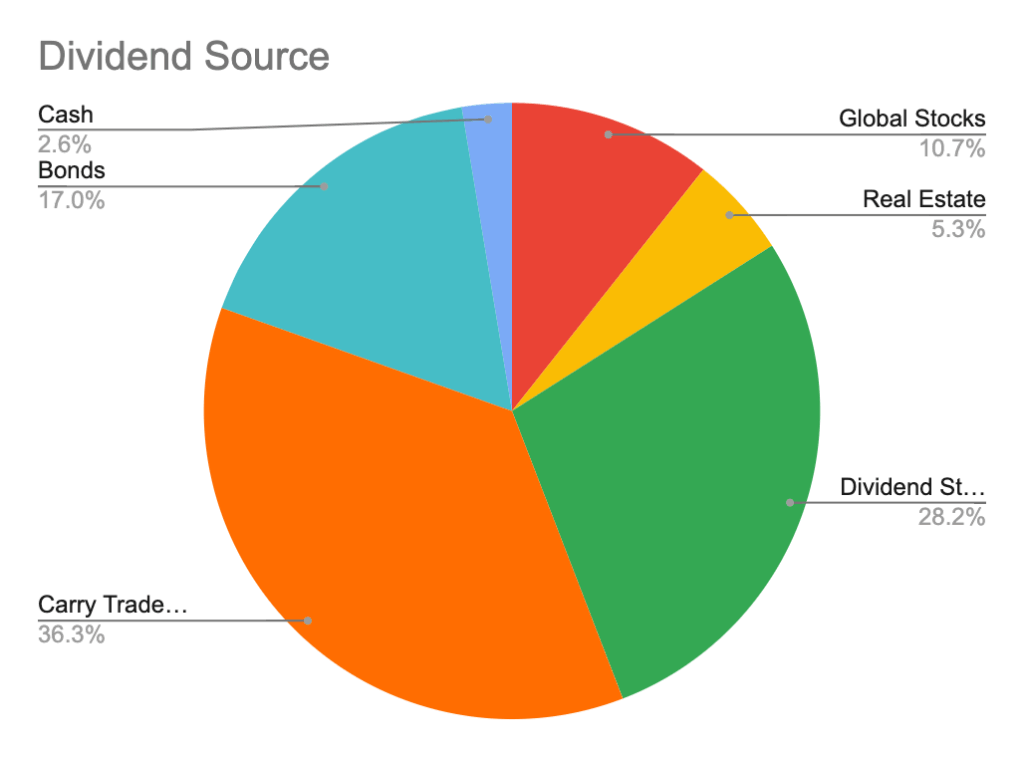

That rounds out my post Bitcoin portfolio, so lets crunch the numbers and see what it looks like. Assuming a five million dollar total portfolio, and numbers from the trailing twelve months.

Yield: 2.76%

Cashflow: $137,784

–Monthly: $11,482

This is north of the rough target of $10k a month I am aiming for, and this is retaining almost half of the entire portfolio in non cash flow yielding bitcoin. This allows me to live entirely from the yield of the portfolio and avoid any asset sales to cover cost of living, which psychologically feels quite satisfying, even if it is the mystical trickery of dividends.

Buying Bitcoin was easy. Holding was harder. Building this machine to live on is the hardest, and possibly most impactful, step yet.