Bitcoin is risky. It’s a volatile asset. even the most ardent bitcoiner would be at pains to deny that (though some do try).

But what occured to me recently is that it would be possible to build a portfolio for any risk appetite, using bitcoin only.

This idea is true of almost any publicly traded asset type that has has derivative products and a sufficiently liquid market, but this is a Bitcoin blog, so that’s what we will focus on in this post.

Through the use of derivative products, it’s possible to build a portfolio that amplifies bitcoin price volatility massively, or even negate it entirely. By combining a blend of these positions, it would be possible to chart a portfolio on a path of almost any risk appetite on that spectrum, and most notably still outperform most other asset classes.

For simplicity in this article we will work with the following assumptions:

- A single bitcoin is priced at $100,000

- The funding rate on Perpetual futures is 10%

- The T-Bill rate, for purposes of the “Risk Free Rate” is 5%

We will model three scenarios covering bitcoin price crashing to $50,000, staying flat at $100,000, and doubling to $200,000.

For each portfolio construct we will also show the Sharpe and Sortino ratios which model out risk and reward and act as a handle on gauging risk appetite. (Sharpe shows returns per unit of volatility. Sortino does the same but only penalises downside moves.)

Volatility metrics are based on historical bitcoin price data (~70% annual).

Spot Bitcoin

The simplest strategy: Buy and hold BTC outright.

In our spectrum of risk, this acts as the middle ground and offers simple price exposure with no derivatives.

With $100,000, you purchase 1 BTC.

| BTC Price | Portfolio Value | Return |

| $50k | $50k | –50% |

| $100k | $100k | 0% |

| $200k | $200k | +100% |

- Expected Return: ~25%

- Volatility: ~70%

- Sharpe Ratio: (25–5)/70 ≈ 0.29 (Excess return divided by volatility)

- Sortino Ratio: (25–5)/50 ≈ 0.40 (Excess return divided by downside volatility)

This offers pure BTC upside but full downside exposure, akin to holding volatile equities. This is the most simple idea and you would be exposed 1:1 with bitcoin price volatility and reward.

Carry Trade

On the most conservative end of the spectrum, you could construct and entirely delta-neutral portfolio that is entirely immune to bitcoin price volatility and simply profits from the funding payments made from people taking long positions on bitcoin price on futures exchanges.

A delta-neutral strategy: Buy 1 BTC spot and short 1 BTC in futures, earning a 10% APR funding yield from the basis (futures premium).

This generates income regardless of BTC’s price direction.

| BTC Price | Portfolio Value | Return |

| $50k | $110k | +10% |

| $100k | $110k | +10% |

| $200k | $110k | +10% |

- Expected Return: 10%

- Volatility: ~5–7%

- Sharpe Ratio: (10–5)/7 ≈ 0.71

- Sortino Ratio: (10–5)/4 ≈ 1.25

In this set up, the trade acts like a synthetic bond providing yield with minimal volatility. The only risk is counterparty risk in holding funds on a crypto exchange, but even this can be mitigated by spreading the trade across multiple exchanges, or keeping the majority of the spot bitcoin in cold storage and maintaining only enough on the exchange to meet your margin.

Futures (2x Long)

On the other extreme end of the spectrum we can use leverage to amplify exposure to bitcoin price and ramp up the level of risk and reward by a multiple, in this case 2x but potentially as high as 50x.

Using $100,000 as collateral for a 2x leveraged long position, you gain exposure to 2 BTC (notional value $200,000).

For enhanced simplicity here, we do not factor in the PERP funding cost of 10%, which would haircut these returns by that much, variable on the volatility over the course of the year.

| BTC Price | Portfolio Value | Return |

| $50k | $0 (liquidated) | –100% |

| $100k | $100k | 0% |

| $200k | $300k | +200% |

- Expected Return: ~50%

- Volatility: ~140%

- Sharpe Ratio: (50–5)/140 ≈ 0.32

- Sortino Ratio: (50–5)/100 ≈ 0.45

This amplifies gains (and losses), similar to high-risk venture bets potential for multiples or total wipeout.

Core Building Blocks

On the most conservative extreme we have a portfolio constructed to return 10% regardless of market price action. This means even if bitcoin price doubles the upside is capped at 10% but in the event the price collapses, the principal is secured and still returns 10%.

On the most risk-hungry portfolio in this scenario we roll the dice on either total wipeout (losing all $100,000 invested) or making a 3x on the total investment and profiting $200,000.

Again, holding simple spot bitcoin sits in the middle of both of these extremes.

Think of spot bitcoin as riding the rollercoaster, futures as standing up with your seatbelt off, and the carry trade as just selling on-ride photographs.

However, what if we take a blended approach between all three portfolios, combining both extreme positions with spot bitcoin, in either direction to marginally increase or decrease risk and return.

Blended Conservative (Carry + Spot)

- $50k in carry: +10% = $55k across all scenarios.

- $50k in spot (0.5 BTC).

| BTC Price | Carry | Spot | Total | Return |

|---|---|---|---|---|

| $50k | $55k | $25k | $80k | –20% |

| $100k | $55k | $50k | $105k | +5% |

| $200k | $55k | $100k | $155k | +55% |

- Expected Return: ~20%

- Volatility: ~35–40%

- Sharpe Ratio: (20–5)/40 ≈ 0.38

- Sortino Ratio: (20–5)/30 ≈ 0.50

Blended Aggressive (Spot + Futures 2x)

- $50k in spot (0.5 BTC).

- $50k in 2x futures (1 BTC exposure).

| BTC Price | Spot | Futures | Total | Return |

|---|---|---|---|---|

| $50k | $25k | $0 (liquidated) | $25k | –75% |

| $100k | $50k | $50k | $100k | 0% |

| $200k | $100k | $150k | $250k | +150% |

- Expected Return: ~40%

- Volatility: ~105%

- Sharpe Ratio: (40–5)/105 ≈ 0.33

- Sortino Ratio: (40–5)/75 ≈ 0.47

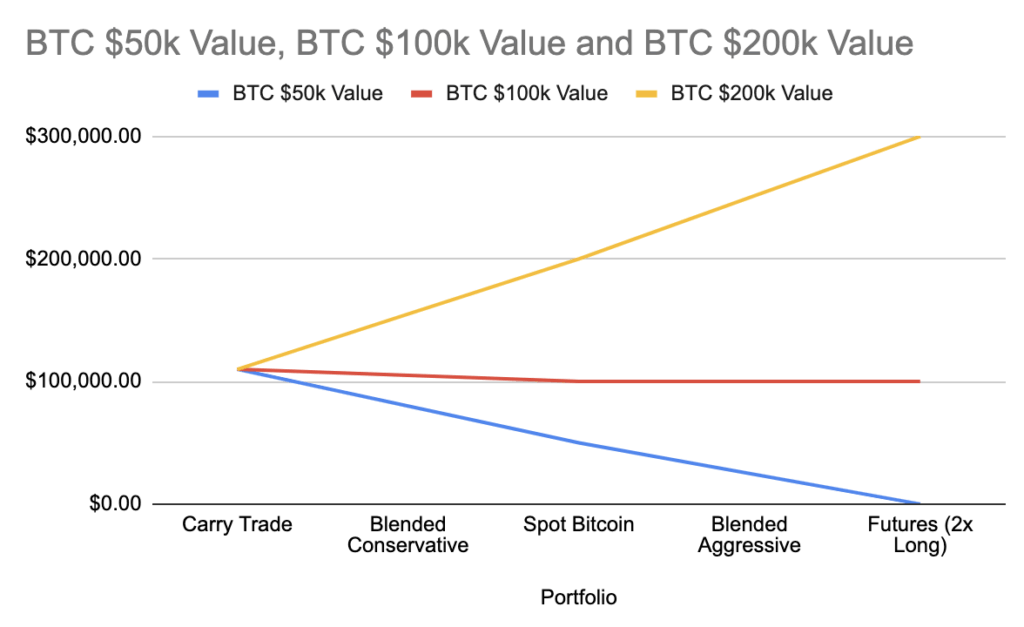

Visualising the Portfolios

If we rank these portfolios from least to most aggressive, and then plot their expected returns based on the three price movement scenarios, we get the following:

As we can see, as we move left to right along the risk appetite spectrum, the potential loss and gain is magnified. The blended conservative portfolio out performs holding spot bitcoin in the price crash scenario, but under performs it in the scenario that the price doubles. This trend continues along the risk spectrum until the Futures 2x long portfolio which completely wipes out in a crash, but outperforms spot bitcoin by $100,000 in the price rising scenario.

What’s also interesting to see is that the expected return in the bitcoin price flat scenario is higher on the conservative end and slopes downward as slide more aggressive in our portfolio. This would actually continue lower if we modelled in funding payments on the two most aggressive portfolios.

The key takeaway: diversification doesn’t need stocks, bonds, or altcoins. With Bitcoin alone, you can dial risk anywhere from “sleep-well-at-night bond” to “Vegas moonshot.” The only question: how much risk do you want to carry?